Have you ever used Quicken 2007's life planning tool.

It's very interesting tool. It takes a bit of work, but can help you determine if your savings plan will work. Granted assumptions like duration of your life (and your spouses) and your long term earnings rate are subject to influences outside of your manageable control, it's still worth knowing. Fidelity is supposed to have a similar tool - that is free - it's a monte carlo simulation designed to analyze the likeliness of your investments growing to the your target amount. Through third parties I have the impression it is less thorough on the expense side. A comprehensive analysis, would probably include both. I'll check it out in the next few months. In Quicken, I assume an 8% rate of return before retirement and 4% after retirement - I believe this is pre-tax (though much of our assets will be tax deffered).

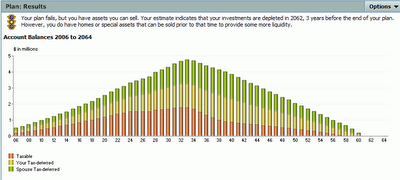

Here is mine:

You'll notice that my plan doesn't carry us for the duration until I am 91 and my wife is 95.

It falls about 3 years short. If we can't change things - such as costs and expenses - we can consider a reverse mortgage, however, I'm not too excited about the thought of burdening our home in our 90s. Will we even be able to do it? Would it be appraised at a fair price?

Utlimately we need to increase our asset aggregation or decrease expenses.

Regards,

makingourway

PS I'll discuss this in more details later.

2 comments:

It seems as though the amount of money you'll have at retirement, combined with the projected length (40 years?) makes 4% a pretty conservative assumption. What if you invest 1/2 of it conservatively and 1/2 of it quite agressively for the first 20 years? That's really a long time frame - you can absorb a lot of ups and downs. If you get even 6% return overall using that strategy, what does it do to your numbers?

Anne,

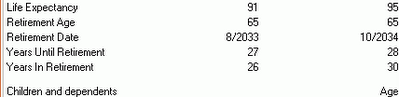

Excellent point, however, I expect to have about 30 years of retirement (or 27), not 40.

Regardless, your point is salient and a good one.

I might raise the % of expected earnings due to the longer number of years. At least 5%. I'll post what I find when the assumptions change.

Regards,

makingourway

Post a Comment