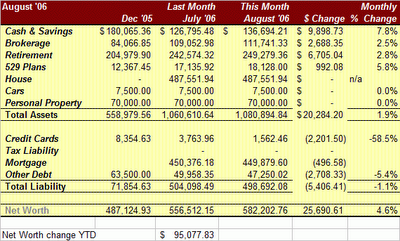

The most significant contributors were:

- reduction in spending lead to increased savings.

- nice gains on investments: 2.5% on brokerage account and 2.8% on retirement account - these are significantly due to the overall market recovery from the April - July doldrums.

- Addition $2000 into retirement accounts ($800 deferal, the rest employer match). My wife's retirement account had healthy gains predominantly due to timing. We accelerated investments in early July in order to take advantage of what we sensed were market lows. In fact, we were a bit early, but the 401k administrator delayed the transaction to a more profitable date.

- Our 529 plans had the healthiest investment increase of about 5.9% (but once you remove the $590 contribution it went down to 2.0%, which is still a nice monthly gain).

- all debt reduction was fairly normal as planned, perhaps more aggressive on the credit cards, but they are paid off regularly each month.

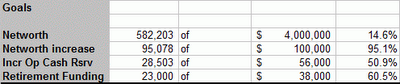

Goals Update

We've made great progress on our networth increase and should exceed it by end of September. In March, 2006, I revised our networth goal to $86,000, but kept the $100k in my blog side board and monthly updates as a stretch goal.

Due to pending medical expenses and related time off (for the new baby), we'll take a cash flow hit of ($21,763). Either I'll have the new job in time to absorb half or all of it, or we'll take it on the chin. We have enough savings to handle it, but of course, we'd rather not dip into them. We may also have some additional paid time off that could alleviate some of the expense, but we won't know until we're deep into it.

Factoring in the $21,763 hit to cash flow as of 12/31/2006. I've calculated our expected increase in networth to be $91,700 for CY 2006. If we do it, it will beat our revised estimate and be close to our stretch. This also assumes we don't spend $3,000 on vacation - which is unlikely.

The total impact will be about $33,500 if we have no offsetting increase in income or reduction in expenses.

If we decide to take a family vacation around Christmas time, that could hit us for another $3k.

I'm confident we'll make the balance up in the following year, by which time I'll have changed to a better job.

Regardless of which, having our new bundle of joy is priceless.

Networth Change Table

Asset Allocation

asset allocation chart here

{kind=link}

Our asset allocation in bonds declined from 8.6% to 8.2%. Almost all bonds are held in our Schwab lifecycle retirement mutual funds (SWERX) plus whatever we have in prosper - I consider prosper junk bonds. The increases in our other equities probably helped drive the number down a bit.

Trading Account Performance

trading account performance chart here

{kind=link}

Our trading account is an expiriment primarily in low cost index ETFs with an allocation model discussed here. As mentioned the delay in liquidating insurance holdings has delayed our achieving our targetted asset allocation. However, as I've read Bernstein's book further, I would change our target asset allocation by adding REITs, more value holdings, international small cap and eventually some precious metal investments (small).

Seeking further international weighting I purchased Morgan Stanley's India Fund (IIF), something I had been waiting to do for a while. It's a closed-end fund (CEF), so it trades like an ETF. The price had dipped low enought to make it worth jumping into. It still trades at a premium to NAV, but I think that's more of a reflection of how difficult it would be to trade directly on Indian markets (from the USA) and obtain diversified holdings.

I'm curious to see what the dividends will be like from the India Fund (IIF) and Russia and Eastern Europe (RNE). Historically they have been fairly high.

My half.com experiment has netted me $326.90 and more importantly freed up some space on one of my bookshelves. Overall about $180 came from selling the extra DVDs I had and $140 from books. Half.com does seem to do better than Ebay. I will reduce prices slowly each month. My last reduction picked up two more buyers for me. I imagine I'll drop prices by about 5% each month until the inventory is cleared or I would do better donating the book.

Thoughts for September

- We will have some interesting expenses for the new child.

- I will increase college savings by about $620 per month starting in September.

- I hope to have the new life insurance policies underwritten and hope, but doubt they will be issued by month's end.

- I will play golf a few times (I played my first partial game last week).

- We will finalize the selection of an investment advisor, sign contracts and begin the creation of an investment plan.

- We will hire a new cleaning person / service and may see our $50/week budget remain the same or double to $100/week. We have found an incredible husband and wife team, but we're not happy with the thought of spending $100/week. We may hire a weekly person and have the team "deep clean" the house one time per month.

- To help with the new baby, we will try to hire a nanny. We have $300 per week budgetted, I assume this is low.

- I will learn more about the Chicago job and continue pursuing a job change.

Have a wonderful weekend,

makingourway

2 comments:

Congrats! Not a bad month at all. Appears as though you have a very hectic 6mos coming if you end up taking the job in Chicago - good luck with it all!

$2m,

Yes not a bad month. Best in a very long time. One day, far in the future, investment gains and losses will far outstretch the impact of savings and reduced spending - but I'll have to save and reduce alot of spending to get there.

Chicago and baby will make a VERY hectic 6 months! Chicago's a far way from happening - still only a possibility - but it did stimulate the idea of nationalizing my search even if I have to commute long distance to home for 6 months!

Have a great holiday weekend,

makingourway

www.makingourwayblog.com

Post a Comment