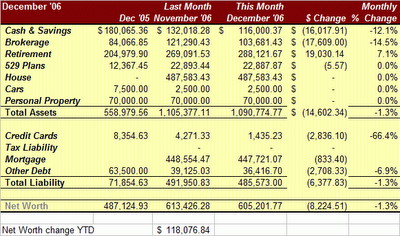

We had quite a few expenses and a significant drop in income in November and December, they were reflected by a $8.2k drop in networth (despite decent investment performance).

The bottom line: The major impacts were $10k in investment charges for liquidating our insurance investments and $8k in asset transfers to our children. Furthermore we accelerated about $7k in expenses from January into December for tax and business reimbursement reasons. Adding back such extraordinary expenses, we would have been up $17k in December, 2006. Details at the end of the posting.

I've put quite a few graphics into this posting and will run commentary after each one.

The following is our Quicken Financial Plan. I increased our retirement investment growth from 4% to 5%. This bought us quit a bit of extra time (more than we plan to be alive). How do I justify the increase? I expect to keep at least 50% of our savings in equities while we're in retirement. The average gain from a diversified equity portfolio should might be about 8%, combined with a fixed income portfolio of maybe 3-4%, should bring us into the 5% range. Furthermore, a large portion of our savings will be outside retirement accounts. We will sell appreciated assets and pay capital gains tax at reduced tax rates compared to regular income. Our model assumes that 100% of our income will be subject to regular income tax.

Bottom line: We are on-track assuming future life assumptions hold.

Here is our month to month net worth update.

Here is our month to month net worth update.This needs some clarification:

1. We spent a lot this month - which reduced our cash. Half of the reduction comes from $8k we put into Custodial Roth retirement accounts for two of our children. Therefore an asset transfer - versus consumptive spending.

2. Our brokerage balance is reduced temporarily. Our insurance assets were liquidated and deposited made into cash accounts. These some of the money is still in transit - in cash accounts - waiting to go into the brokerage accounts. The brokerage balance does not reflect that.

3. Great gains on our retirement accounts. I've liquidated most of them into cash pending asset transfers from Schwab to Vanguard.

4. We continue to reduce our other debt. By March we should have eliminated the other debt (except for some interest free loans which we will maintain).

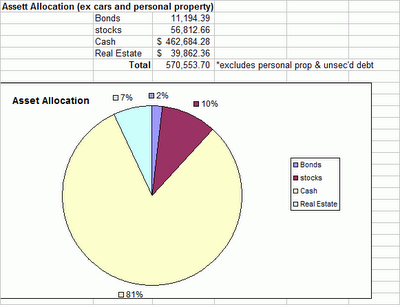

Our asset allocation, below reflects the massive move into cash necessitated by the account transfers between brokerage firms (Schwab and Bright Start to vanguard). Prosper has become a significant component of our bond holdings.

Below is a value list and performance chart of our trading account. We now have two main trading accounts. This one will soon be closed and moved over to Vanguard. All the funds shown are ETFs except for India fund (IIF) and easteru euro (RNE), which are closed end funds.

I plan to liquidate the holdings this year and integrate the money into our investment plan. Overall performance was not far off from the s&p 500 (annualized) - considering these investments were made in April 2006.

Here is a summary of our goals and goal performance. Some, like Networth, are long term goals, while others, such as Networth increase are short term. We're doing well on the networth increase, but our cash reserve can certainly do better. It will be a challenging goal for next year with the move and job changes. We will be a single income family for at least two and a half months during my wife's job change.

The following is an overview of our investments in prosper.com. Over the last few months I've largely ignored prosper out of frustration with the high demand / increased efficiency for good credit loans. Rates are dropping far too quickly from opening bid amounts. Prosper is too new for me to feel comfortable investing in low credit loans until there's enough credit history in place for a prosper specific contextual analysis.

One reason my cash balance is higher is due to a defaulted loan that was repaid in full - I'm still having trouble understanding how that happened (100%)?

Here is an overview of our prosper accounts. Please note the portfolio distribution is skewed toward higher grade borrowers. Despite that, we're making fairly high interest rates. I don't expect to put much more money into prosper next year with our new expenses coming and the illiquidity of prosper loans. I will probably put more in 2008. I will reinvest loan proceeds.

This chart documents loan performance.

Not bad 15.61% APY rivals the S&P 500, providing I don't have further defaults. Which would be better putting the money into the s&p 500 or keeping it here?

Discussion of major expenses and analysis of drop in networth

- The insurance companies hit us with $10,000 in surrender charges when we liquidating our variable and whole life policies. I view this as a short term sacrifice - in exchange I can invest in low cost index funds at 0.25% expense ratios (ERs) versus 2.5% from the variable policies. I also now have twice the insurance at a fixed cost for the next 30 years.

- We transferred $8000 to our children - who worked in our family business - and put the money into custodial Roth ira's. We're hoping the retirement money will be far enough away that they do not dip into it in their late teens or twenties. Paying for college and helping our children save for retirement are personal priorities for my wife and myself.

- Our Chicago month-long business trip/vacation cost about $5,000 - for 2/3's of which I can receive reimbursement in January.

- I have a number of other expenses I expect reimbursement for in January. The expected total will run about $7k.

- We did have some extraordinary expenses. My wife and I each bought new eyeglasses and updated prescriptions in our old pairs. The cost was $1900. It's quite a bit, but I figure eyeglasses are the one piece of clothing you wear almost every day - they should look good.

- We had a $500 last minute Christmas gift from polo.com that should be offset by returning a $350 gift (this is part of the$7k back in January).

- We made a second mortgage payment this month, which we will not have to make in January in order to accelerate the tax deduction (already in the$7k).

Thoughts for January

- We should receive $7k in a combination of reimbursements, returns and reduced expenses.

- Quicken projects we'll have an extra $11-$12k in cash flow provided no extraordinary expenses - since we'll both be working

- We will have $1000 in legal fees for my wife's contract with the new employer

- My wife is scheduled for a small $1,000 bonus

- We have requested about $3,000 in healthcare reimbursements from my wife's employer. About $2,000 will actually be asset transfers from accounts accruing flex spending and dependent care spending

The next four months will be a critical period for my wife and I to save as much as possible before she takes several months off again. With both our incomes chugging at full blast I'm hoping we can position ourselves strongly for the move, house purchase, house sale and new job.

Have a great January.

Regards,

makingourway

2 comments:

makingourway,

I am really curious how people employee their children so that they can make Roth contributions (I'm thinking ahead ;-) - if your willing - I would love to hear how you approached this......

$2m,

I would examine how your children could provide administrative, clerical or maintenance support for your burgeoning real estate business.

Collecting leaves, filing papers, throwing out the trash, all things even young ones can do.

Regards,

m

Post a Comment