1. web business are less tangible, they often have lower start-up costs than businesses requiring large capital investments - some borrowers have less respect for credit

2. he borrowed the money for a business, rather than the business borrowing it directly. he may be willing to sacrifice his credit to support the continuity of the business - perhaps it's not doing well.

3. he let the debt go past 30 days and maybe have bounced one or more checks to prosper - it was hard to tell in the update.

Defaults are to be expected and statisticly should conform to real world default experience. Default rates need to be factored into lending rates.

I've changed my bidding philosophy and approach. I now bid now earlier than the last day of the auction. This means daily review of open auctions, but it saves the incredible amount of time wasted on most rebidding.

I've transfered another $500 into prosper to bring my account closer to $2000. When our family finances improve, I'll try to increase the rate of investment to bring our portfolio closer to $10,000.

I also plan to examine www.zopa.com and www.kiva.org as alternatives to prosper. I might pick up new lending strategies.

I may restrict my lending amounts to $50 for anything borrowers B grade or less - I seem to be using this approach instinctively.

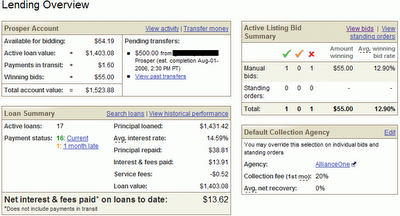

Here is a summary of my portfolio:

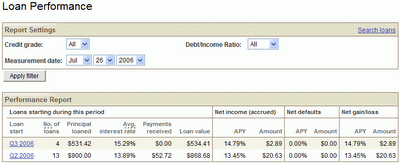

Here are the details of my loan performance:

In light of the possibility of loan default, I examined prosper's rules regarding defaults - rule#1 is essentially, don't contact the borrower due to debt collection laws, etc.... Here are some of the relevant rules:

[blogger won't let me upload the third pic, so I'll try to edit the posting and re-post it tomorrow]

All in all my average interest rate is moving up over 14%. If you consider real inflation somewhere between 3 - 5%, it's a pretty good net interest rate, even after adjustments for risk.

According to Bernstein, the stock market is expected to move at 3.5% real rates for the immediate future a 8 - 10% real return is pretty attractive by comparison.

Have a wonderful weekend,

makingourway

www.makingourwayblog.com

4 comments:

What are the timeframes on your loans? How long do borrowers have to pay them back? Are the timeframes on loans all the same, or is that part of the bidding process?

Everyone posting about Prosper seems to be complaining about defaults. The question is whether on a risk adjusted basis it outperforms alternative investments? Especially also considering the time needed to make lots of those $50 investments.

Justin,

prosper loans are 36 pmt 3 year loans. They can pay early without penalty.

regards,

makingourway

www.makingourwayblog.com

moom,

defaults are something you need to factor into your interest rates. even after factoring in the varying default rates, most loans exceed an 8% nominal return.

as to the time the $50 investments cost to make, my thoughts are:

a. make $100-$200 investments on anything b grade or better.

b. use discipline to scan auctions quickly

c. use tools to help analyze and bid to save time.

despite that, with a $10k-$20k investment base you'll probably spend 4-8 hours per month in order to earn $100-$300 in interest. based on the value of your time and competing interests, it's your call.

regards,

makingourway

www.makingourwayblog.com

regards,

makingourway

Post a Comment