five cent nickel, raised a very interesting question last week on his blog regarding a possible work around for retirement contribution limits.

To selectively quote him, he's concluded:

...The upshot was that if you have any self-employment income (like ad revenue from blogging), you can open a SEP-IRA and then make contributions to it as your own employer. This shields your earnings from both income tax and self-employment tax....

SEP contributions do not count against your limit for Traditional or Roth IRA

contributions. So you can max out your regular IRA and contribute to a SEP. But

wait! It gets better… You can also rollover your SEP IRA into your Traditional

or Roth IRA.

I'm not an accountant, but I have been both self-employed and owned various businesses. My past experience is somewhat different than five cent's hypothesis, which is quite intriguiging, and causing me to hope that I am indeed wrong.

The following is my evolved analysis of the strategy:

The key consideration for evaluating five cent's plan is how much you earn. Your earnings effect:

- your eligibility to participate in a roth ira

- the deductability of your traditional ira contribution (you can always make it)

- your ability to roll over a SEP into a roth plan

I own a business and have made individual 401k and SEP IRA contributions in different years. Currently I prefer individual 401ks because you can put the first $15k (this year) earned without having to worry about the 25% income limitation of SEPs.

You can’t put more than 25% of your income into a SEP up to a maxmimum of $44,000 in 2006. Check with your accountant, but my research below indicates that you can deduct 1/2 the self-employement tax, but not all of it. Also, the maximum you can put in the SEP is reduced by the amount you put into your employer's 401k.

My updated points:

a. Employment Tax on contributions - you might be able to make larger overall contributions due to the SEPs higher limit, but you will still have to pay self-employment tax — check this out with a CPA to see if I’m right (I could be wrong). If you're also contributing to a 401k at work, the 401k contribution (I had mistyped it as 410k contribution limits) will reduce what you can put into the SEP IRA.b. SEP IRA - SEP IRA contribution will not count against your ROTH IRA contribution, since a ROTH is made with post tax dollars, however, your actual income level will directly effect if you can participate in a Roth plan. Check with your CPA, but my research indicates that if you earn more than $100,000 you can't rollover your SEP into a Roth that year.

c. Traditional IRA - I am pretty sure a SEP IRA will not prevent you from contributing to a traditional IRA, however, you are more than likely to lose the deductability of your traditional IRA contribution. I maxed out my individual 401k contribution and made a traditional IRA contribution that my CPA determined was not tax deductible, although it's earnings will grow tax deferred.

Since contributions are reported annually,the IRS will know about this matter and

decide if it’s a mistake or not - so I recommend a CPA decide it for you

before the IRS does.d. Why rollover into a traditional IRA? I think fivecent has a great idea rolling over into a ROTH plan - especially if you're skeptical about future tax rates, but I don't think you have any increased benefits by rolling your SEP plan into a traditional IRA. In fact, you may have increased benefits by keeping the SEP plan distinct. Certain retirement plans, such as 401ks, rollover IRAs and maybe SEPs, have unlimited protection against creditors, while traditional IRAs have $1M protection against creditors (I'm not an attorney, so check this out with yours before making any decisions and to confirm if I'm right). I wonder if you lose the unlimited protection by rolling a SEP IRA into a Roth?

Conclusion: I think the key take away is that you can probably roll a SEP IRA into a Roth, pay the taxes the conversion process requires (i.e. the income tax that a SEP normally shields you from) and enjoy the money tax free in your retirement if you make less than $100k that year. You'll still pay self-employment tax, but receive a deduction for 1/2 of it.

Interesting relevant research:

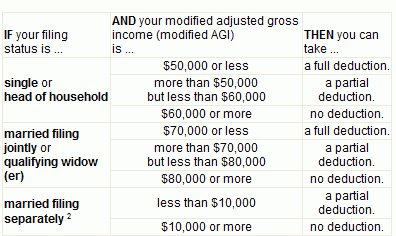

The following is a link to the IRS bookloet on IRA accounts booklet 590. What's relevant to the discussion is that traditional IRA deductability is phased out at the following income levels if you are covered by an employer retirement plan (this is from the 2006 publication):

Here the IRS says you can contribute, but if you're over the limit, it's not deductible:

Nondeductible Contributions

Although your deduction for IRA contributions may be reduced or eliminated, contributions can be made to your IRA of up to the general limit or, if it applies, the spousal IRA limit. The difference between your total permitted contributions and your IRA deduction, if any, is your nondeductible contribution.

Also, here's something else interesting, to rollover to a Roth, you must have an AGI of less than $100,000. The following is from the same publication:

Converting From Any Traditional IRA Into a Roth IRA

You can convert amounts from a traditional IRA into a Roth IRA if, for

the tax year you make the withdrawal from the traditional IRA, both of the

following requirements are met.Your modified AGI for Roth IRA purposes

(explained in chapter 2) is not more than $100,000. You are not a married

individual filing a separate return.

The is the link for document 560,which discusses SEP IRA plans. It looks like the $15k elective deferal limit a 401k is subject to (the remaining contributions must be profit share from the employer) may not be in effect any longer for self employed with SEP IRAs -- however, you still have the $42k (or 25% of income) overall limit for all defined contribution plans.

One interesting point it makes when discussing net income is the following:

Net earnings from self-employment.

For SEP and qualified plans, net earnings from self-employment is your gross income from your trade or business (provided your personal services are a material income-producing factor) minus allowable business deductions. Allowable deductions include contributions to SEP and qualified plans for common-law employees and the deduction allowed for one-half of your self-employment tax.Net earnings from self-employment do not include items excluded from gross income (or their related deductions) other than foreign earned income and foreign housing cost amounts.

For the deduction limits, earned income is net earnings for personal services

actually rendered to the business. You take into account the income tax

deduction for one-half of self-employment tax and the deduction for

contributions to the plan made on your behalf when figuring net earnings.

This sounds like you can get credit for 1/2 of the self-employment tax (paid to social security, etc...).

The last paragraph is the one that excited fivecent:

A SEP-IRA cannot be designated as a Roth IRA. Employer contributions to a SEP-IRA will not affect the amount an individual can contribute to a Roth IRA.

Contribution Limits

Contributions you make for 2005 to a common-law employee's SEP-IRA cannot exceed the lesser of 25% of the employee's compensation or $42,000 ($44,000 for 2006). Compensation generally does not include your contributions to the SEP.

This paragraph is an important one, it says your SEP and 410k contributions cannot exceed $42,000 or 100% of your income (I assume the $42k increases to $44k for 2006).

More than one plan. If you contribute to a defined contribution plan (defined in chapter 4), annual additions to an account are limited to the lesser of $42,000 or 100% of the participant's compensation. When you figure this limit, you must add your contributions to all defined contribution plans. Because a SEP is considered a defined contribution plan for this limit, your contributions to a SEP must be added to your contributions to other defined contribution plans.

4 comments:

Interesting. I am just beginning to explore my options with the small amount of self employment income I am getting. I am currently leaning towards an individual 401(k) over a sep ira.

2million,

I strongly recommend the individual 401k. The most compelling reason is this:

You can contribute your first $15,000 of income earned this year, regardless of the % of income you earned - this is a beautiful bypass of the 25% of income restriction.

Keep in mind, however, that it's still a defined benefit plan per the IRS and there is an aggregate limit if you're contributing to other defined benefit plans, such as a 401k at work, or a SEP IRA.

Have a great day,

Making Our Way

What you meant in your last paragraph is it's still a defined contribution plan ( not a defined benefit plan).

Another benefit of the Solo 401k plan is that the pretax deferrals are taken out of the gross income before you figure the self employment tax. Unfortunately the profit sharing component is not, but, as you indicate, it is tax deductible.

Additionally, the Solo 401k can allow for loans from your account should you need some additional capital for your business. And you can do the loan without needing any credit score. Also, you repay the loan to your own account so the interest repaid is really all yours.

These are some of the benefits that the administrators over at http://www.solo-k.com suggest.

Hi there,

You made a comment to http://www.bargaineering.com/articles/primer-on-self-employment-taxes-or-why-sep-iras.html saying "The most recent IRS guidelines no longer distinguish between employer and employee contributions to a SEP, which makes a lot of sense, since the self-employed can arbitrarily recategorize them. There is still the overall limit of $44,000 (this year) or 25% of your salary." Can you provide a reference that confirms this? I made an employee contribution to my SEP IRA (combined employer and employee contributions are under the employer limit) and am desperately trying to find out whether the IRS will categorize the employee contribution as a traditional IRA contribution and thus not deductible under the deduction phaseout rules in table 1-2 from http://www.irs.gov/publications/p590/ch01.html#d0e2185.

Post a Comment